RoadBuddy provides independent information to help drivers compare auto insurance options with confidence. We may earn a commission when you click on partner links, but this never affects our reviews or recommendations. Our content is researched and published independently.

Car Insurance Coverage Types: How to Choose the One You Really Need

Published 14.01.2026 | 8 min read

Advertiser Disclosure

RoadBuddy is a free resource that helps drivers compare auto insurance options.

We may receive compensation from some insurance companies and partners when you click on links or request a quote through our site. This may affect where offers appear, but it does not influence our reviews, guidance, or editorial decisions.

Our content is researched and written independently to give you clear and unbiased information.

By using RoadBuddy, you acknowledge and accept this disclosure. Learn more.

The question “Do I need insurance?” is a simple and obvious one, but it is only when you think about how it is really not a simple question of yes or no, and that whether you are legally required to have insurance, whether you are required to have insurance from your lender, and whether you can afford it all depend on a variety of factors that you can appreciate the complexity of the question that is being asked.

The difference between having the bare minimum and having enough, and the difference between having too much and having too little, can be significant indeed.

Does Your State Require Insurance?

In almost all states, you are legally required to have some kind of automobile insurance in order to drive. The only state that does not require this is the state of New Hampshire, where you are allowed to drive without it as long as you have some other kind of financial responsibility.

In the other states, the kind of insurance that you are legally required to have is liability insurance. This kind of insurance will cover any injuries or damages that you may cause to others in the event of an accident. This is required in all states except New Hampshire.

The amount of liability coverage varies from state to state. The minimum amount of coverage may be $15,000 per person for bodily injury in some states. In other states, it may be as high as $50,000 or more. Some states may require additional types of coverage.

The penalties for driving without insurance can include heavy fines. The fine may range from hundreds of dollars to as much as $5,000. Your license may be suspended, your car may be impounded, and you may have to carry an SR-22 form.

If you are involved in an accident and are uninsured, you will be responsible for all of the damages. This means that you will be responsible for any medical expenses, car repairs, attorney fees, and even a lawsuit that could result in garnishment of your wages. What may seem like a cost-effective choice, being uninsured, could end up being a financial burden that could cost you much more than the cost of insurance.

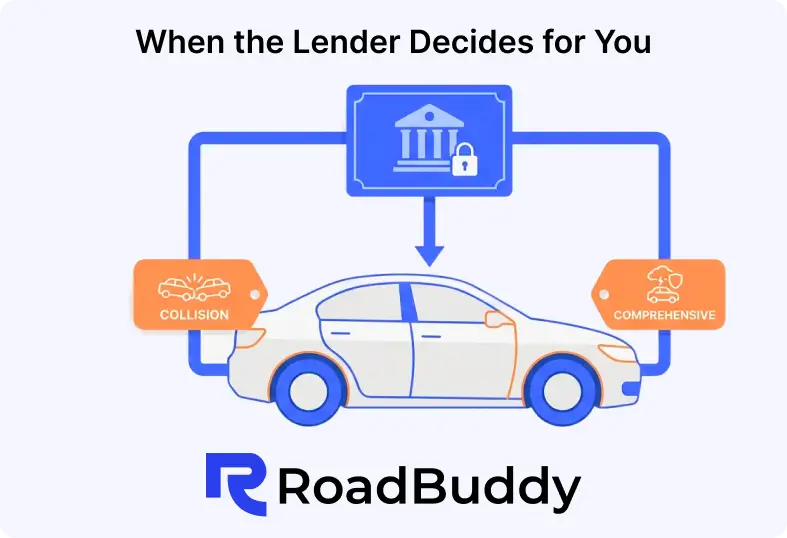

When Your Lender Requires More Than the Minimum

If you financed the vehicle through a bank, credit union, or dealership, that institution has a financial interest in that vehicle. They want to protect their investment. This means that the loan agreement on that vehicle probably requires that you carry both collision and comprehensive insurance, as well as liability.

Same situation applies if you’re leasing. The leasing company owns the vehicle, and they require specific coverage to protect their asset. In most cases, leases require collision and comprehensive coverage with deductibles no higher than $1,000.

Here’s the important part: this isn’t optional. If you don’t purchase the required coverage yourself, your lender or leasing company will purchase it on your behalf and add the cost to your monthly payment. Usually at rates much higher than what you’d pay for it yourself.

If you’re unsure what collision and comprehensive coverage actually include, understanding the difference helps you make better decisions about whether the coverage your lender requires is appropriate for your situation.

For financed vehicles, the lender typically requires this coverage to stay on your policy until the loan is paid off. Once the loan is satisfied and you own the car outright, you can choose whether to keep or drop these coverages.

For leased vehicles, comprehensive and collision coverage are usually required for the entire lease term. When the lease ends and you return the vehicle, you no longer need that coverage (assuming you’re not buying the lease).

Make Sure You’re Not Overpaying

You’ll be redirected to our partner’s site to get offers.

Advertiser Disclosure

RoadBuddy is a free resource that helps drivers compare auto insurance options.

We may receive compensation from some insurance companies and partners when you click on links or request a quote through our site. This may affect where offers appear, but it does not influence our reviews, guidance, or editorial decisions.

Our content is researched and written independently to give you clear and unbiased information.

By using RoadBuddy, you acknowledge and accept this disclosure. Learn more.

Owned Vehicles: When You Make the Decision

Once you have paid off the loan on your car or never had a loan on your car, the decision on what kind of insurance to carry is up to you. The minimum liability required by your state will still be required, but the optional coverages of collision and comprehensive will be up to you.

So, what makes sense for you?

If your car is new or has significant value, then carrying collision and comprehensive insurance makes sense. If your car gets damaged in an accident or stolen, the cost of fixing or replacing the car would be a significant expense if you didn’t have insurance.

If your car is old and has little value to begin with, then the numbers work out differently. If your car is worth $3,000 and you’re paying $1,200 per year for full coverage, then you’re paying 40 percent of your car’s value to have it fully covered. In this case, it’s common to have liability coverage on your vehicle and to self-insure it by having the money set aside to fix it if need be.

The choice to have it or not to have it comes down to whether or not you can afford to replace your vehicle. If you can afford to replace your vehicle, then you probably don’t need to have it insured. If you cannot afford to replace your vehicle, then it’s probably best to have it insured regardless of how old it is.

Make Sure You’re Not Overpaying

You’ll be redirected to our partner’s site to get offers.

Advertiser Disclosure

RoadBuddy is a free resource that helps drivers compare auto insurance options.

We may receive compensation from some insurance companies and partners when you click on links or request a quote through our site. This may affect where offers appear, but it does not influence our reviews, guidance, or editorial decisions.

Our content is researched and written independently to give you clear and unbiased information.

By using RoadBuddy, you acknowledge and accept this disclosure. Learn more.

Special Coverage Types and When They Matter

Beyond liability, collision, and comprehensive, there are several other coverage options that sometimes make sense depending on your situation.

Uninsured/Underinsured Motorist Coverage (UM/UIM)

This covers you if someone without adequate insurance hits you. If you’re injured or your car is damaged by an uninsured driver, this coverage pays for your expenses instead of requiring you to sue the other driver.

Some states require this coverage, others make it optional. If your state doesn’t require it but you live in an area with a high percentage of uninsured drivers, it’s worth adding. The premium for this coverage is usually modest but can save you substantial money if you’re hit by an uninsured driver.

Personal Injury Protection (PIP) or Medical Payments Coverage

These cover your medical expenses after an accident regardless of fault. PIP covers medical bills plus lost wages and other accident-related expenses. Medical Payments coverage covers just medical expenses.

Some states require one or both of these, others don’t. If your state doesn’t require them but you don’t have good health insurance, these can be worth adding because they’ll pay your immediate medical expenses if you’re injured in an accident you didn’t cause.

Gap Insurance

Gap insurance covers the difference between what you owe on your car loan and what your car is actually worth if it’s totaled.

Here’s when it matters: When you first finance a car, you often owe more than it’s worth. A $30,000 car depreciates quickly—by year two it might be worth $22,000 even though you still owe $25,000. If that car is totaled, your regular insurance pays $22,000 (the car’s value), but you still owe $25,000 on the loan. Gap insurance covers that $3,000 difference.

Gap insurance only matters in total loss situations—not for regular accidents or repairs. It also only matters while there’s actually a “gap”—once your car is worth more than you owe on the loan, gap insurance becomes irrelevant.

Most people only need gap insurance for the first 2-3 years of a loan, which is when the gap between loan balance and car value is largest. Many dealers try to sell gap insurance to everyone, but for someone keeping a financed car for five years, gap insurance for all five years is unnecessary and wasteful.

Whether your lease requires gap insurance varies by leasing company, but many leases do require it.

Rental Car Reimbursement

This covers a rental car when your car is in for repairs from an accident. There is usually a limit for each day (such as $30 per day) and a limit for the entire rental period (such as $900 total).

You would need this if you cannot afford to be without a car while your car is in for repairs. If you work from home or if you can get to work by public transportation, then you probably do not need this. If you need your car for work, then this may be something you should consider.

Roadside Assistance

This includes towing, fixing a flat tire, locksmith assistance, and jump-starts when you are traveling. This is very affordable (typically $5 to $15 per month) and can end up saving you money if you have a breakdown when you are away from home or if you don’t have AAA membership.

Whether or not you should purchase this is based on the age of your car and how much you trust it.

The Reality of Minimum vs. Recommended

This is what insurance experts recommend and what your state requires:

Your state may require bodily injury liability coverage of $25,000 per person, but insurance experts recommend $100,000 or more depending on your assets. Why? Because if you cause an accident that injures someone and your liability coverage is not enough to cover the expenses, the injured person may sue you for the difference. This is a problem if you have assets to protect.

Likewise, your state may not require that you carry the uninsured/underinsured motorist coverage or the personal injury protection coverage, but it is good to have it if you live in a high area of uninsured motorists or have no good health insurance.

It’s the difference between “minimum requirements” and “actual protection” that gets a lot of people into trouble. They may think they are insured, but then find out the hard way that the minimum amount is not enough when they get into a lawsuit that is more than they have.

Make Sure You’re Not Overpaying

You’ll be redirected to our partner’s site to get offers.

Advertiser Disclosure

RoadBuddy is a free resource that helps drivers compare auto insurance options.

We may receive compensation from some insurance companies and partners when you click on links or request a quote through our site. This may affect where offers appear, but it does not influence our reviews, guidance, or editorial decisions.

Our content is researched and written independently to give you clear and unbiased information.

By using RoadBuddy, you acknowledge and accept this disclosure. Learn more.

Making the Decision: A Practical Framework

Start by understanding what your state requires, because that’s the legal baseline. If you’re financing or leasing, add whatever your lender requires. Then consider:

- How old is your vehicle?

- What’s it actually worth right now?

- Could you afford to replace or repair it without insurance?

- Do you have good health insurance for medical costs?

- What percentage of your annual income would a major lawsuit cost?

- Do you live in an area with high uninsured driver rates?

Your answers to these questions determine what coverage actually makes sense for your situation. Someone financing a new car should carry close to full coverage because they have a financial obligation to the lender and the car’s value justifies it. Someone driving a ten-year-old paid-off car with solid emergency savings might reasonably carry liability-only.

Both are making smart decisions, just different ones based on their real-world circumstances.

The answer to the question of when you need to have coverage depends on where you live, whether you owe money on your car, what you can afford, and what kind of risks you are willing to take. By understanding these factors, you are able to make a decision that really works for you, as opposed to what someone else says you need to carry.

🛡️ Car Insurance Asset Protection Calculator

Answer 3 quick steps to get a personalized coverage recommendation based on your net worth and risk profile.

Step 1Your Assets

Step 2Your Debts

Step 3Risk Profile

ResultsYour Coverage

Calculate Your Total Assets

Enter approximate values. These are for coverage estimation only — not stored or shared.

$

$

$

$

$

$

$

$

Total Assets

$0

⚠️ Retirement accounts: 401(k)/ERISA plans have strong federal protection. IRAs vary by state — some states cap protection at $1M, others offer partial or no protection.

Subtract Your Debts

We'll subtract these to calculate your net worth — the number that determines how much you have to protect.

$

$

$

$

$

$

Total Assets$0

Total Debts$0

Estimated Net Worth

$0

💡 Under 40? We'll add 3 years of gross income to your net worth for coverage purposes — your future wages can be garnished in a lawsuit judgment.

Your Personal Risk Profile

5 quick questions to calibrate your coverage recommendation.

1. How many miles do you drive per year?

2. Where do you primarily drive?

3. Who else drives your vehicle(s)?

4. What is your driving record over the last 3 years?

5. What type of vehicle(s) do you drive?

Moderate Risk

100/300/100

Recommended Liability Limits (BI per person / BI per accident / PD)

🔍 Get Quotes for My Coverage

Compare rates from top carriers based on your recommended limits — free, no obligation

Your Risk Profile

Moderate

Bodily Injury

$100,000 / $300,000

Per person / per accident for injuries you cause to others

Property Damage

$100,000

Damage to other vehicles or property you cause

UM / UIM

$100,000 / $300,000

Protects you when hit by uninsured or underinsured driver

Est. Net Worth Protected

$0

Your estimated net worth + income exposure covered

| Coverage | Recommended | Status |

|---|

⚠️ This calculator provides general educational guidance only — not personalized legal or financial advice. Coverage needs vary by state, individual circumstance, and policy terms. Consult a licensed insurance professional for personalized recommendations.

Looking for Auto Insuranse?

Make sure you’re not overpaying

You’ll be redirected to our partner’s website to compare personalized offers.

Advertiser Disclosure

RoadBuddy is a free resource that helps drivers compare auto insurance options.

We may receive compensation from some insurance companies and partners when you click on links or request a quote through our site. This may affect where offers appear, but it does not influence our reviews, guidance, or editorial decisions.

Our content is researched and written independently to give you clear and unbiased information.

By using RoadBuddy, you acknowledge and accept this disclosure. Learn more.