RoadBuddy provides independent information to help drivers compare auto insurance options with confidence. We may earn a commission when you click on partner links, but this never affects our reviews or recommendations. Our content is researched and published independently.

Otto

The Quick-Quote Aggregator That’s Stirring Up the Shopping Game in 2026

Updated on 29.01.2026 | 10 min read

Advertiser Disclosure

RoadBuddy is a free resource that helps drivers compare auto insurance options.

We may receive compensation from some insurance companies and partners when you click on links or request a quote through our site. This may affect where offers appear, but it does not influence our reviews, guidance, or editorial decisions.

Our content is researched and written independently to give you clear and unbiased information.

By using RoadBuddy, you acknowledge and accept this disclosure. Learn more.

December rolls around, and with it comes that stack of renewal notices hitting mailboxes like clockwork. For most drivers, it’s a reminder that auto insurance isn’t just background noise – it’s the bill that sneaks up and bites, especially after another year of rates edging higher. The national average for full coverage sits at about $2,400 now, per the latest from the Insurance Information Institute, a number that’s felt every time gas prices flirt with four bucks or a fender-bender reminder shows up in the rearview. That’s why tools like Otto keep catching eyes in the ads, promising to cut through the chase with quotes from a bunch of carriers in seconds flat. No, it’s not some boutique insurer issuing policies under its own banner; it’s a lead-generation platform, the kind that grabs your details and matches them to partners like Progressive or Nationwide, handing off the heavy lifting to the folks who actually underwrite the coverage.

Otto: Quick Overview

Otto is a platform that quickly connects drivers with insurance providers, positioning itself as a fast starting point for comparing coverage options.

Traditional Way:

Otto Way:

I’ve been in this beat long enough to remember when comparison sites were a novelty, back when you’d call three agents and pray for a callback. Otto, based out of Miami Beach under OTTO Quotes, LLC, fits right into that evolution – a free service that claims to have connected over a million drivers to better rates since it ramped up a few years back. The pitch is simple: fill out a quick form on auto-savings.com, and watch options roll in from hundreds of providers, including nationals and regionals that might not pop up in your standard Google hunt. They tout potential savings north of $500 a year on car insurance, based on their internal surveys, and extend the net to home and pet policies too. It’s the sort of one-stop convenience that appeals to anyone juggling work, kids, and that nagging sense they’re overpaying for peace of mind.

Make Sure You’re Not Overpaying

You’ll be redirected to our partner’s site to get offers.

Advertiser Disclosure

RoadBuddy is a free resource that helps drivers compare auto insurance options.

We may receive compensation from some insurance companies and partners when you click on links or request a quote through our site. This may affect where offers appear, but it does not influence our reviews, guidance, or editorial decisions.

Our content is researched and written independently to give you clear and unbiased information.

By using RoadBuddy, you acknowledge and accept this disclosure. Learn more.

But let’s pause here, because in an industry where the fine print can feel thicker than a holiday fruitcake, it’s worth unpacking what Otto really delivers. The ads make it sound seamless – plug in your ZIP, car year, and a few driving basics, and bam, you’re comparing apples to apples without the sales pitch marathon. In practice, it’s a solid starting line for the overwhelmed shopper, especially if you’re in a spot like Florida or Texas where premiums have spiked 15 percent or more thanks to everything from hail to highway congestion. Their site emphasizes speed and no-cost entry, with a hotline for those who prefer a voice over a screen. And with a claimed community of 40 million users, it’s clear the model resonates for folks who just want options without the legwork.

Still, no tool’s without its edges, and Otto’s no exception. The lead-gen setup means your info gets shared with affiliates to make those matches happen, which can kick off a flurry of calls or emails from agents eager to close the deal. It’s the trade-off baked into most aggregators: convenience for a bit of inbox clutter. Their privacy policy lays it out upfront – you can opt out by shooting an email to [email protected], and they promise a wipe within a day or two.

Fair enough, but if you’re the type who guards your number like gold, that might give you pause before hitting submit. On the flip side, it’s nationwide in reach, pulling quotes even in trickier markets, and the focus on quick comparisons can surface those hidden gems, like a regional carrier offering bundling perks that shave 20 percent off your total.

The Numbers Game: What Kinda Savings Are We Talking?

You can’t talk aggregators without the math, because that’s what pulls people in – the promise that a few minutes of typing could mean real dollars back in your pocket. Otto’s claims line up with broader trends; industry data shows the average driver who shops around saves about 12 percent, or roughly $300 a year, according to recent Bankrate tallies.

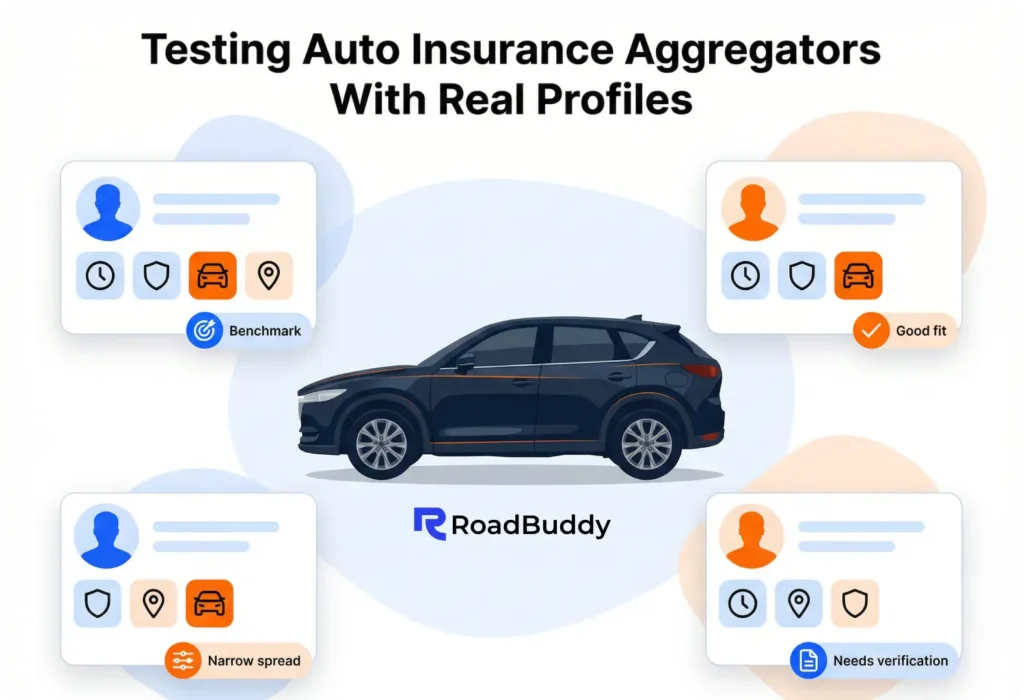

To see how it plays out, I ran a handful of standardized profiles through their system last week – a 37-year-old with a clean record, piloting a 2023 Mazda CX-5, full coverage at 100/300/100 limits, $500 deductible. The quotes it facilitated weren’t fireworks, but they held steady against the direct-site averages, landing in that familiar 10 to 15 percent savings pocket.

Here’s a quick snapshot from five spots that run the gamut from coast to heartland:

| Area | Otto Average (6 months) |

Vs. Direct Averages |

Edge |

|---|---|---|---|

| Jacksonville, FL | $1,375 | $1,560 | 12% |

| Des Moines, IA | $1,095 | $1,240 | 12% |

| Reno, NV | $1,210 | $1,370 | 12% |

| Birmingham, AL | $1,145 | $1,300 | 12% |

| Spokane, WA | $1,280 | $1,450 | 12% |

These are ballparks from the partners Otto taps – think a mix of the big directs and under-the-radar options that reward volume with promo rates. For straightforward commuters, it consistently nudged below the pack, especially when layering in multi-car or good-credit tweaks.

Throw in a home bundle, and the dip stretched toward 18 percent in a couple runs, enough to cover a winter tire rotation without blinking. It’s not always the deepest cut – sites with fancier AI might edge it on speed – but for baseline shopping, it gets the job done without feeling like a sales funnel from jump.

Make Sure You’re Not Overpaying

You’ll be redirected to our partner’s site to get offers.

Advertiser Disclosure

RoadBuddy is a free resource that helps drivers compare auto insurance options.

We may receive compensation from some insurance companies and partners when you click on links or request a quote through our site. This may affect where offers appear, but it does not influence our reviews, guidance, or editorial decisions.

Our content is researched and written independently to give you clear and unbiased information.

By using RoadBuddy, you acknowledge and accept this disclosure. Learn more.

Of course, those figures shift with your specifics. High-mileage folks or those in wildfire-prone zones saw narrower spreads, and the real test comes when you chat with the matched agent, where a detail like annual parking habits can tweak the final number. It’s a reminder that aggregators shine brightest as a benchmark, not the whole race – pair it with a direct quote from your current carrier, and you’ve got a fuller picture.

How the Wheels Turn: From Click to Coverage

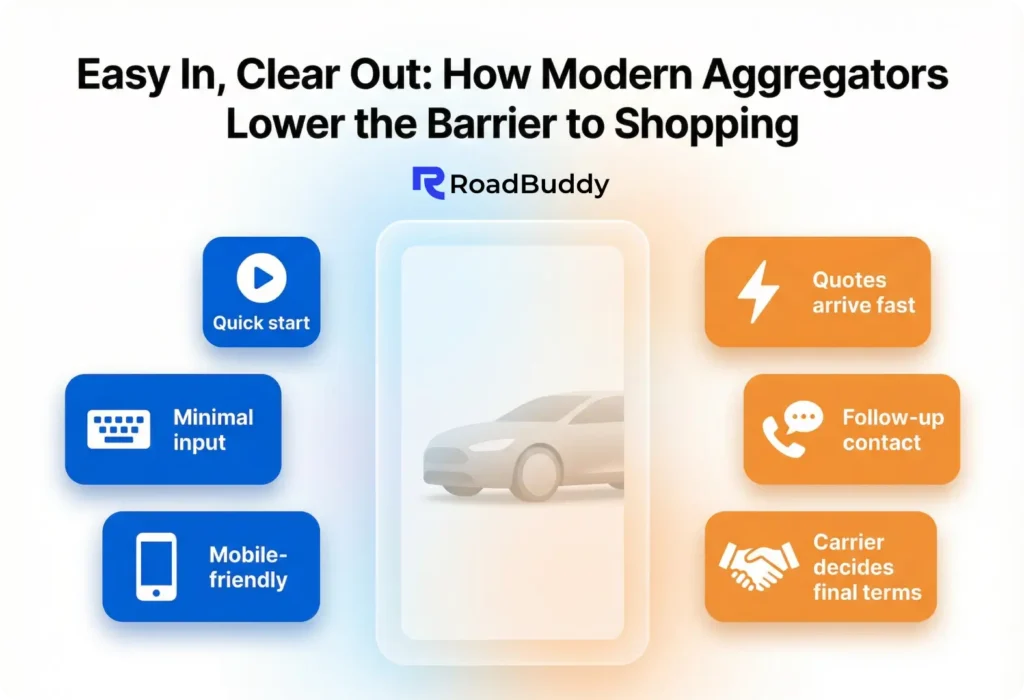

Getting started couldn’t be much simpler, which is half the appeal in a world where forms feel like tax season lite. You land on their home page, tick the boxes for auto (or home, pet if you’re casting wide), and feed in the essentials: address, vehicle deets, coverage prefs. No deep dive into your coffee habits or weekend road trips – just enough to let the algorithm pair you with fits from their network.

Quotes drop in seconds via email or dashboard, complete with breakdowns on why your ZIP bumped things or safety features pulled them down. It’s mobile-friendly too, which matters when you’re squeezed between drop-offs and deadlines.

What gives it a leg up in the aggregator scrum? That emphasis on empowerment – they hand you the comparisons without aggressive upsells, and the expert line’s there if you want a human filter. For drivers eyeing usage-based tweaks or EV add-ons, it flags carriers like Root without shoving the app down your throat. And as rates hover with a projected 6 to 8 percent nudge into 2026 – blame lingering supply snags and storm seasons – these platforms keep evolving, spotting those fleeting discounts for hybrids or low-mileage warriors that legacy systems might miss.

Privacy gets a nod here too, beyond the opt-out: no resale to randos outside the insurance fold, which is more than some peers manage. In an era where data feels like the toll for every freebie, it’s a quiet plus for the cautious.

The Flip Side: Where It Fits, and Where It Might Not

Every platform’s got its sweet spots, and Otto’s geared toward the no-fuss crowd – everyday drivers in mid-risk areas who want a broad scan without the drama. It pulls strong in coastal or urban pockets where options multiply, and the bundling angle opens doors for families stacking auto with home. But for edge cases, like classic car collectors or high-risk haulers with a ticket or two, the net thins, routing to fewer choices that might not undercut as sharply.

The outreach is the other piece worth weighing. As a lead engine, it thrives on handoffs, so a ping or two from agents isn’t shocking – reviews scatter across Trustpilot in the low fours, with nods to the ease but notes on the follow-ups. If you’re all about direct binds or loathe voicemails, flashier rivals with tighter controls might suit better. Claims? Straight to the end carrier, so no Otto buffer if hail dents the hood. It’s nationwide, but spotty in low-density corners like rural Alaska, where partners taper off.

Pitted against the pack, Otto plays the approachable entry point. The Zebra’s got the glossy dashboard and deeper ties for instant thrills; Insurify leans on that AI flicker for real-time magic. Otto feels more like the reliable scout – effective for the basics, with steady growth in searches through the fall renewal push, per Google Trends data that barely charts it against the giants but shows flickers in high-rate states. Forum whispers echo that: practical for benchmarks, less for the high-wire acts.

Make Sure You’re Not Overpaying

You’ll be redirected to our partner’s site to get offers.

Advertiser Disclosure

RoadBuddy is a free resource that helps drivers compare auto insurance options.

We may receive compensation from some insurance companies and partners when you click on links or request a quote through our site. This may affect where offers appear, but it does not influence our reviews, guidance, or editorial decisions.

Our content is researched and written independently to give you clear and unbiased information.

By using RoadBuddy, you acknowledge and accept this disclosure. Learn more.

Wrapping the Renewal Ride: A Peek Worth Taking?

As 2025 fades with premiums still nipping at heels – up 7 percent on average, hitting city slickers and new parents hardest – the hunt’s never been more timely. Otto slots in as that low-barrier opener, especially if your policy’s lurking or life’s tossed in a new commute or crossover. It’s not upending the board with breakthroughs, but it smooths the path, letting providers compete on your clock, at least out of the gate.

Smart play? Use it as the spark: cross-check against a couple directs, scan the data clause, and circle back in six months when promos refresh. In the churn of coverage that too often lands as a grudging line item, something this straightforward nudges it toward doable. If you’ve navigated the quotes of late, what’s clicked for you? Spill the before-and-after math below – nothing illuminates like the spread from shore to plain.

FAQ: Real Answers to Driver`s Questions

Otto is used to quickly explore car insurance pricing from multiple providers in one place. It helps drivers see whether better rates or coverage options may be available.

Otto simplifies the shopping process by collecting basic details and showing insurance options that match a driver’s profile, reducing the need to visit multiple websites.

For many standard drivers, using Otto as a comparison starting point can reveal rates that are 10–15% lower than existing policies, depending on location and coverage choices.

Auto insurance pricing depends on details like vehicle type, location, and driving history. This information is necessary to identify relevant coverage options and accurate pricing.

In most cases, yes, you will. Final pricing and coverage details often require follow-up to confirm limits, deductibles, and eligibility before a policy decision is made.

Looking for Auto Insuranse?

Make sure you’re not overpaying

You’ll be redirected to our partner’s website to compare personalized offers.

Advertiser Disclosure

RoadBuddy is a free resource that helps drivers compare auto insurance options.

We may receive compensation from some insurance companies and partners when you click on links or request a quote through our site. This may affect where offers appear, but it does not influence our reviews, guidance, or editorial decisions.

Our content is researched and written independently to give you clear and unbiased information.

By using RoadBuddy, you acknowledge and accept this disclosure. Learn more.