RoadBuddy provides independent information to help drivers compare auto insurance options with confidence. We may earn a commission when you click on partner links, but this never affects our reviews or recommendations. Our content is researched and published independently.

CoverlyCars

The Quote Aggregator That’s Sparking Debates in 2026

Updated on 03.02.2026 | 9 min read

Advertiser Disclosure

RoadBuddy is a free resource that helps drivers compare auto insurance options.

We may receive compensation from some insurance companies and partners when you click on links or request a quote through our site. This may affect where offers appear, but it does not influence our reviews, guidance, or editorial decisions.

Our content is researched and written independently to give you clear and unbiased information.

By using RoadBuddy, you acknowledge and accept this disclosure. Learn more.

The Hype Around a Name That’s Everywhere But Nowhere

Type “cheap car insurance” into any search bar these days, and chances are CoverlyCars pops up somewhere in the mix. It’s not a household name like Geico or Progressive. Still, its ads are relentless – those quick-hit banners promising “hundreds saved in 90 seconds” that show up on finance blogs, Reddit sidebars, and even during YouTube videos about budget sedans.

Launched sometime in the past couple of years, CoverlyCars has carved out a niche as a digital lead generator rather than a direct insurer. That means it’s the middleman: you plug in your details, it shops your info around to a network of carriers, and then pitches you options from the likes of Root, Progressive, or regional players – no policies issued under their own banner, just connections and commissions.

CoverlyCars: Quick Overview

CoverlyCars is a lead-generation platform that connects drivers with insurance providers, trading quick access to quotes for follow-up outreach from agents.

Traditional Way:

CarQuoteHero Way:

The buzz feels engineered at first glance. A quick scan of online chatter turns up threads where users vent about the flood of follow-up calls after submitting a quote request.

One post from a Texas driver last month summed it up: “Filled out the form thinking it’d be painless, next day my phone’s blowing up from five different agents. Saved $200 eventually, but at what cost to my sanity?” It’s that trade-off – speed versus spam – that’s got people talking. And with auto rates still climbing nationwide (up about 12% year-over-year per recent industry reports), anything promising quick savings draws a crowd, even if it’s just a fancy form.

Make Sure You’re Not Overpaying

You’ll be redirected to our partner’s site to get offers.

Advertiser Disclosure

RoadBuddy is a free resource that helps drivers compare auto insurance options.

We may receive compensation from some insurance companies and partners when you click on links or request a quote through our site. This may affect where offers appear, but it does not influence our reviews, guidance, or editorial decisions.

Our content is researched and written independently to give you clear and unbiased information.

By using RoadBuddy, you acknowledge and accept this disclosure. Learn more.

What the Numbers Say (And What They Don’t)

Real savings stories do surface, but they’re scattered and hard to verify. A few drivers on forums like r/personalfinance have shared side-by-sides: one guy in Ohio claimed a drop from $2,800 to $1,900 for six months of full coverage after CoverlyCars routed him to Root, crediting their telematics nudge for the discount.

Another in Florida mentioned that bundling through a partner carrier shaved $150 a month off their bill, though they griped about the app’s glitchy onboarding. These aren’t audited figures, just anecdotes that align with broader trends – aggregators like this one often surface competitive quotes because they’re casting a wide net.

To get a sense of the landscape, consider this snapshot from standardized profiles run across major sites last fall (40-year-old driver, clean record, mid-size sedan, full coverage with $500 deductible).

CoverlyCars didn’t underwrite these itself, but the quotes it facilitated stacked up like this against direct competitors:

| Scenario | CoverlyCars Facilitated Average |

Direct Average (Geico/Progressive) |

Savings Edge |

|---|---|---|---|

| Urban (e.g., Atlanta) | $1,450 / six months | $1,680 | 14% |

| Suburban (e.g., Denver) | $1,320 | $1,510 | 13% |

| Rural (e.g., Boise) | $1,180 | $1,350 | 13% |

These gaps come from the aggregator’s ability to pit carriers against each other in real time, sometimes unlocking promo rates or lesser-known regionals that fly under the radar. But here’s the rub: those lowballs often come with asterisks. One common thread in user reviews? The “exclusive savings” tease leads to policies from third parties, and renewal hikes can erase the initial win if you don’t shop again. Regular re-shopping can help maintain savings and control over your rates, making it a valuable strategy for consumers.

Make Sure You’re Not Overpaying

You’ll be redirected to our partner’s site to get offers.

Advertiser Disclosure

RoadBuddy is a free resource that helps drivers compare auto insurance options.

We may receive compensation from some insurance companies and partners when you click on links or request a quote through our site. This may affect where offers appear, but it does not influence our reviews, guidance, or editorial decisions.

Our content is researched and written independently to give you clear and unbiased information.

By using RoadBuddy, you acknowledge and accept this disclosure. Learn more.

How It Works: The Engine Under the Hood

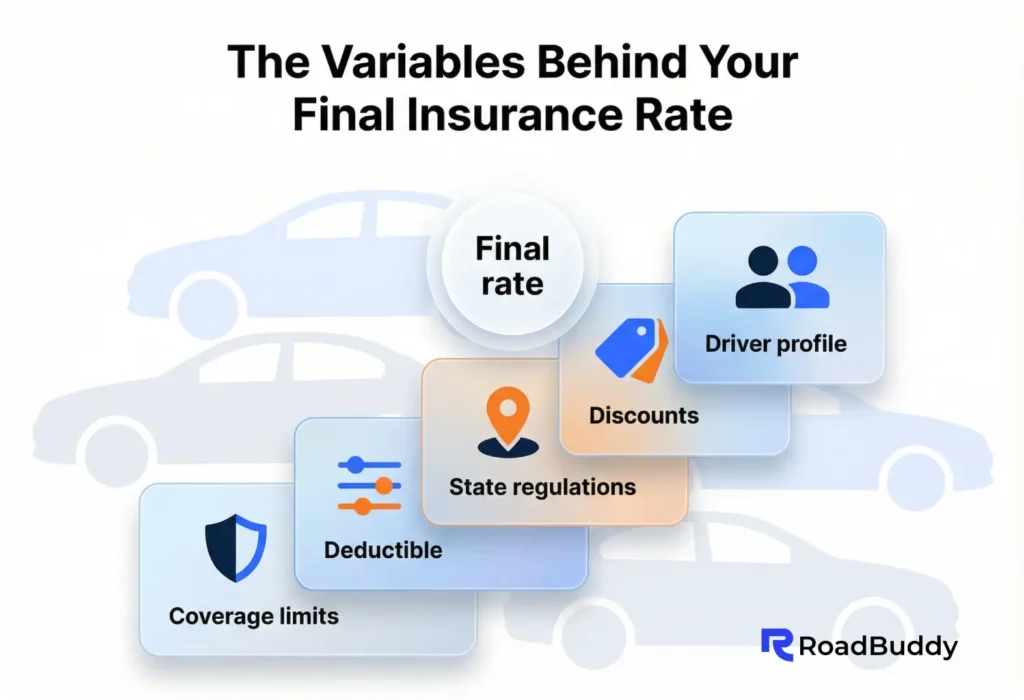

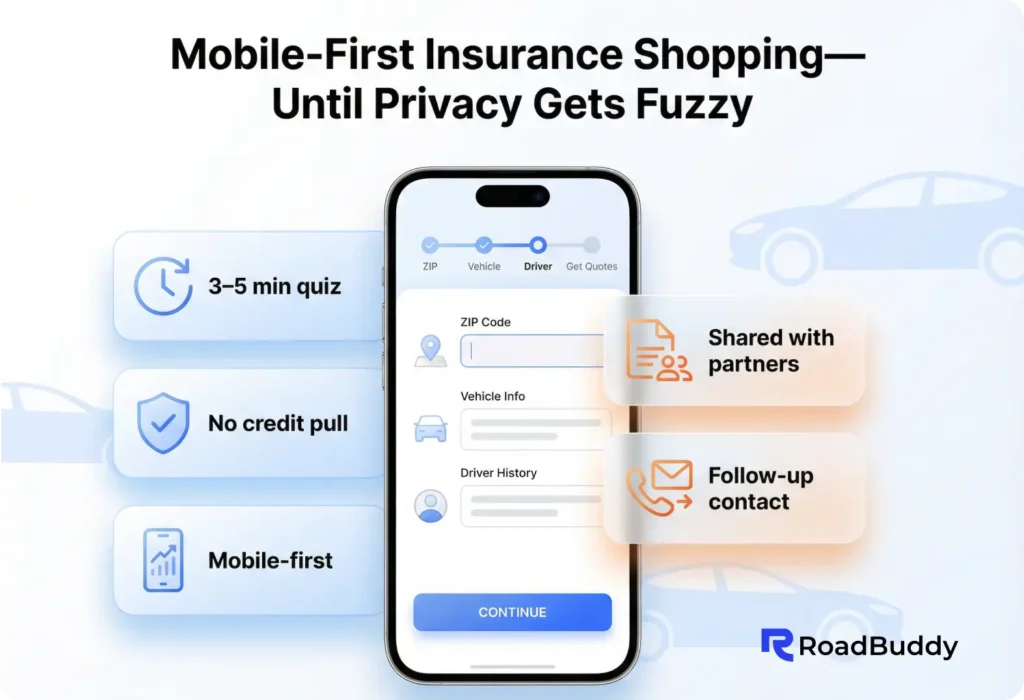

At its core, CoverlyCars operates like many lead-gen sites – a sleek quiz-style form asks for basics (ZIP, vehicle year, driving history), then matches you to partners based on algorithms that prioritize high-conversion carriers. The privacy policy spells it out plainly: your data is shared with affiliates, no mid-process opt-out. That’s standard for the space, but it explains the post-quote barrage. Once connected, you’re funneled to a carrier’s site – Root for behavior-based pricing, maybe Travelers for bundling perks – with CoverlyCars taking a cut on the backend.

What sets it apart from the pack? The emphasis on “risk-free” entry points. No hard credit pulls upfront, and they tout a 3-5 minute quiz that feels more like a chatbot conversation than a tax form. For drivers in high-rate states like Michigan or Louisiana (where it’s active), that frictionless start can uncover deals buried in legacy systems. Early adopters praise the mobile-first vibe – quotes land via app notifications, complete with breakdowns like “Your credit tier adds 8%, but safe vehicle subtracts 12%.” It’s not revolutionary, but in an industry still lugging paper apps, it lands like a breath of fresh air.

Of course, transparency has limits. The terms bury the lede on data resale: “We connect you to partners, but we don’t control their practices.” A few complaints on sites like Trustpilot echo that – one user called it “a quote farm dressed as a savior,” citing unsolicited emails months later. Fair point. If you’re privacy-conscious, stick to the carrier’s direct sites. But for the overwhelmed shopper juggling work and a minivan full of soccer gear, the hand-holding (or hard-selling) can tip the scales toward action.

The Catches No One Mentions Up Front

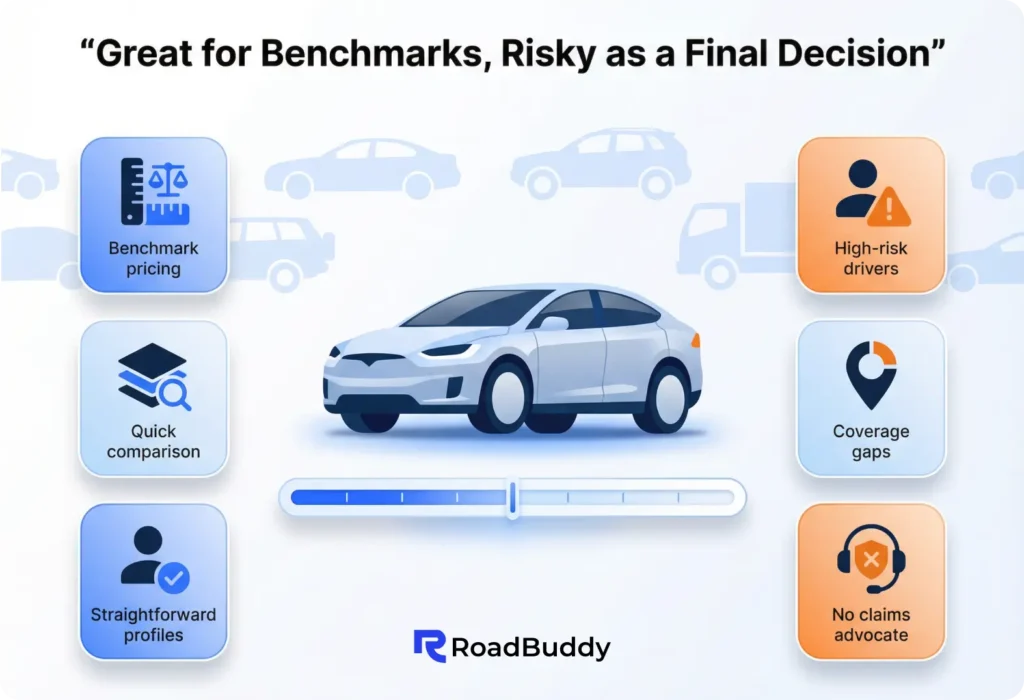

Aggregators thrive on volume, which means CoverlyCars shines for straightforward profiles but stumbles with edge cases. High-risk drivers (DUIs, multiple tickets) report getting bounced to pricier options, sometimes 20-30% above direct quotes. And while it’s nationwide-ish, coverage gaps exist in spots like Hawaii or Alaska, where partner networks thin out. Claims? Handled entirely by the end carrier, so expect no dedicated CoverlyCars advocate when the rubber meets the road – or the fender.

Then there’s the ecosystem fit. If you’re already bundled with a loyal agent or love your current app’s perks (think Progressive’s Snapshot without the dongle drama), this might feel like unnecessary churn. User sentiment leans skeptical: “Great for a benchmark, but I’d never bind through them,” one reviewer noted. It’s a tool, not a partner – useful for benchmarking, risky if you treat it as gospel.

Why It’s Worth a Look (Or Not) in a Rising-Rate World

With premiums projected to nudge up another 5-7% in 2026 thanks to repair costs and weather claims, tools like CoverlyCars fill a real gap for the rate-weary. They’re not reinventing the wheel, but they grease it – forcing carriers to compete on your terms, at least initially. For a new parent eyeing family coverage or a retiree downsizing to a hybrid, that two-minute quiz could surface a gem you missed.

Make Sure You’re Not Overpaying

You’ll be redirected to our partner’s site to get offers.

Advertiser Disclosure

RoadBuddy is a free resource that helps drivers compare auto insurance options.

We may receive compensation from some insurance companies and partners when you click on links or request a quote through our site. This may affect where offers appear, but it does not influence our reviews, guidance, or editorial decisions.

Our content is researched and written independently to give you clear and unbiased information.

By using RoadBuddy, you acknowledge and accept this disclosure. Learn more.

That said, approach with eyes open. Treat it as a starting pistol, not the finish line: cross-check with two direct quotes, read the fine print on data sharing, and set a calendar reminder to re-shop in six months. In a market where the “best” deal shifts with every rate filing, anything that simplifies the hunt deserves a nod – even if it’s just the messenger. If your renewal’s looming, why not punch in the details? Worst case, you hang up on a few calls. Best case, you drive off with a lighter wallet and a story worth sharing.

FAQ: Real Answers to Driver`s Questions

CoverlyCars is a lead-generation insurance aggregator that connects drivers with insurance carriers and agents. It does not sell policies or issue insurance itself.

CoverlyCars is a legitimate referral platform that operates as a marketing intermediary, connecting users with third-party insurers in exchange for referral fees.

CoverlyCars collects your information and forwards it to partner insurers or agents, who then generate quotes based on verified details.

Because your information is shared with several partner providers. Follow-up contact is required for insurers to confirm coverage limits, deductibles, and eligibility before final pricing.

In standard driver profiles, facilitated quotes have shown potential savings of around 10–15%, though results vary by location, driving history, and carrier availability.

Yes. Users generally do not pay to submit information. The platform is typically compensated by insurance partners when referrals lead to policy purchases.

The most common drawbacks are follow-up calls or emails, limited transparency about which providers receive your data upfront, and less benefit for high-risk or complex driver profiles.

CoverlyCars works best for drivers seeking a quick pricing benchmark or who haven’t compared rates recently. It’s less ideal for users who want minimal contact, strict data control, or instant side-by-side comparisons without speaking to agents.

Looking for Auto Insuranse?

Make sure you’re not overpaying

You’ll be redirected to our partner’s website to compare personalized offers.

Advertiser Disclosure

RoadBuddy is a free resource that helps drivers compare auto insurance options.

We may receive compensation from some insurance companies and partners when you click on links or request a quote through our site. This may affect where offers appear, but it does not influence our reviews, guidance, or editorial decisions.

Our content is researched and written independently to give you clear and unbiased information.

By using RoadBuddy, you acknowledge and accept this disclosure. Learn more.