RoadBuddy provides independent information to help drivers compare auto insurance options with confidence. We may earn a commission when you click on partner links, but this never affects our reviews or recommendations. Our content is researched and published independently.

How to Lower Your Car Insurance: 47 Proven Strategies (Ranked by Savings Potential)

Published 09.03.2026 | 15 min read

Advertiser Disclosure

RoadBuddy is a free resource that helps drivers compare auto insurance options.

We may receive compensation from some insurance companies and partners when you click on links or request a quote through our site. This may affect where offers appear, but it does not influence our reviews, guidance, or editorial decisions.

Our content is researched and written independently to give you clear and unbiased information.

By using RoadBuddy, you acknowledge and accept this disclosure. Learn more.

Lower car insurance has become a straightforward budget problem in 2026. Depending on the dataset and driver profile, national averages for full coverage cluster roughly between about $2.1k and $2.7k per year, which means even a 10% improvement can translate into meaningful annual savings.

The runner-up to the quest for affordable car insurance rates is the query of why did my car insurance rates increase. The reason for this is that your car insurance rates may change even if your driving habits have not. This is because car insurance companies reprice due to increased costs of repairing vehicles, increased compensation for injuries, theft, and changes in weather-related claims in your area. In most states, your car insurance rate will change based on non-driving factors such as credit-based insurance scores and loss trends by territory.

This guide ranks 47 strategies by savings potential, so you can start with the highest-impact changes first. Realistically, the right combination often adds up to $200 to $1,500+ per year depending on your state, vehicle, and starting price point.

Each strategy is scored using the same ranking system: effort level, implementation time, and typical savings percentage range. You will also see state-specific tactics and stacking rules, because the best results usually come from combining a few strong moves rather than relying on a single change.

How to Use This Guide

Use this list as a build-your-own car insurance savings checklist. Each tip has three categories so you can focus on quick wins and not waste time: effort level, timeframe, and a savings percentage range.

Effort levels are easy to understand. Low effort means you can accomplish it quickly with little hassle. Medium effort means you’ll have to shop around, get some information, or make a change to a policy. High effort means it’s a bigger decision, such as changing cars, changing how you use your cars, or adjusting coverage on multiple policies.

Timeframes are categorized into immediate actions, improvements that typically take one to three months to show results, and long-term moves that require six months or longer to appear.

The savings percentage ranges are estimates and not guarantees. They are presented in ranges based on state regulations, carrier pricing, and your current premium. The ordering emphasizes approaches that generally yield the greatest and most consistent savings.

Immediate Wins (0-7 Days)

Switch Insurance Carriers

Shopping for insurance is still the fastest way to lower your rate because different insurance companies do not charge the same driver the same rate. The best time to shop for car insurance quotes is at renewal, right after a life change that affects your risk (move, new car, new driver, mileage increase), and at least once a year even if you haven’t changed anything. Although shopping for insurance outside of these times can still work well for you, you will get the best apples-to-apples comparison when your policy is set to automatically renew.

When switching insurance companies, do not make these two errors, which will void your savings. First, do not have any gaps in coverage, even if it is only for a brief time, because this will cause you to be placed in higher pricing tiers in the future. Second, do not choose the lowest premium without checking basic financial stability ratings and complaints, because a low premium is not worth much if the claims service is substandard. Watch for potential pitfalls in getting quotes, such as higher deductibles than you now have, lower liability limits, missing rental car coverage, or reducing uninsured motorist coverage to lower the premium.

Strategy #1: Get 5+ quotes online (Effort: Low | Time: 1-2 hours | Savings: 15-40%)

Use the same limits and deductibles for all quotes so you are comparing price, not altering the product. If a quote is significantly lower, make sure it didn’t sneak in lower liability limits or higher deductibles.

Strategy #2: Use independent insurance agents (Effort: Low | Time: 2-3 days | Savings: 10-35%)

An independent agent can give carriers quotes that you may not always be able to find on your own and can point out underwriting information that can cause fluctuations in pricing, such as previous insurance continuity, garaging address, and driver assignment.

Strategy #3: Consider regional carriers vs. national brands

Regional carriers can be more competitive in certain states because they specialize in local risk and have different expense structures. The trade-off is that availability is limited by state, and you still need to check financial strength and service reputation before switching.

Make Sure You’re Not Overpaying

You’ll be redirected to our partner’s site to get offers.

Advertiser Disclosure

RoadBuddy is a free resource that helps drivers compare auto insurance options.

We may receive compensation from some insurance companies and partners when you click on links or request a quote through our site. This may affect where offers appear, but it does not influence our reviews, guidance, or editorial decisions.

Our content is researched and written independently to give you clear and unbiased information.

By using RoadBuddy, you acknowledge and accept this disclosure. Learn more.

Adjust Your Deductibles

Raising a deductible is one of the cleanest ways to reduce a premium because you are essentially agreeing to pay more out of pocket before the insurance company will pay. The downside is that the savings may be limited if you already have a high deductible, and it may not be the best strategy if you don’t have the money on hand when a claim occurs. This isn’t also the best strategy for older cars where collision claims are more likely to result in a borderline repair, since a high collision deductible may make small to medium losses feel like you are self-insuring anyway.

Strategy #4: Increase collision deductible to $1,000 (Effort: Low | Time: 1 day | Savings: 10-25%)

This tends to produce the biggest deductible-driven drop because collision is usually the more expensive physical damage coverage. Make the change only if paying $1,000 without stress is realistic for you.

Strategy #5: Increase comprehensive deductible (Effort: Low | Time: 1 day | Savings: 5-15%)

Comprehensive claims are often theft, glass, hail, or animal-related, so you are betting you can absorb the deductible if something happens. Some people keep comp deductible lower than collision because comp losses can be more random and region-dependent.

Strategy #6: Emergency fund requirement calculation

Before you raise anything, set a minimum cash buffer equal to your highest deductible plus at least one month of essential expenses. If you have separate collision and comprehensive deductibles, assume the higher one. If you cannot cover that amount from savings today, lowering the premium by raising the deductible is usually a false economy.

Remove Unnecessary Coverage

The quickest way to reduce a bill is to simply stop paying for coverage that you do not need anymore. This is where the term “drop full coverage” is often improperly used, as liability-only insurance can be a good idea for some vehicles and a bad financial decision for others. The question is collision coverage worth it for your vehicle now, not what you paid for it years ago.

Strategy #7: Drop collision on cars worth under $3,000 (Effort: Low | Time: 1 day | Savings: 20-40%)

But if your car is not worth much, then collision may often become a bad bargain because one accident can ruin your car and the payment will be reduced by your deductible. One simple rule of thumb is this: if the maximum realistic payment after the deductible would not change your financial situation, then collision is probably optional. You should keep liability coverage because that is the insurance that will protect you from having to pay for the damage and injuries you cause.

Strategy #8: Remove rental car coverage if you have alternatives (Effort: Low | Time: 1 day | Savings: 5-10%)

Rental reimbursement is useful when you would be forced to rent during repairs, but many people already have a backup vehicle, can carpool, or can work remotely. Some credit cards and certain auto clubs also provide limited rental benefits, so check before paying twice.

Strategy #9: Eliminate roadside assistance and use an AAA-style alternative (Effort: Low | Time: 1 day | Savings: 2-5%)

Roadside add-ons are convenient, but they are rarely the best value. An auto club membership can offer broader towing and lockout coverage, and it follows you rather than the car, which is helpful if you drive multiple vehicles.

Update Your Mileage

Annual mileage is one of the simplest pieces of information to use to base premiums on, as it is a direct indicator of risk. The less you drive, the less opportunity there is for an accident to happen, so premiums are often based on mileage and include a low mileage discount if you qualify in a lower mileage band.

Strategy #10: Report reduced commuting and work-from-home changes (Effort: Low | Time: Same day | Savings: 5-15%)

If you changed to telecommuting, hybrid days, or a shorter commute, you’ll need to update your annual mileage estimate and ensure that the primary use category for the vehicle is accurate. Additionally, some carriers will rate the vehicle differently depending on whether it is used for business, commuting, or pleasure.

Strategy #11: Consider usage-based insurance programs (Effort: Medium | Time: 3-7 days | Savings: 10-30%)

Usage-based insurance policies factor in driving habits and mileage recorded through an app or device. They offer significant discounts to drivers who are low-mileage and smooth, but they are not a blanket success. If you are a late-night driver, a stop-and-go commuter, or a frequent hard-braker in heavy traffic, this service will cut you off from the discount or simply void it altogether.

Quick Policy Adjustments (1-30 Days)

Discount Optimization

Think of discounts like tags in a database. If the tag is missing, you do not get paid for being eligible, and nobody alerts you. The fastest savings here usually comes from verifying what is already supposed to apply to you, then stacking the discounts your carrier allows.

Strategy #12: Multi-car discount (Effort: Low | Time: 1 day | Savings: 10-25%)

If you have more than one car, it may be cheaper to combine them rather than having separate policies. This is most effective if all the drivers are fairly insurable, as having one bad driver can raise the rates.

Strategy #13: Paperless and auto-pay discount (Effort: Low | Time: Same day | Savings: 2-5%)

Small but consistent. Turn it on and confirm it shows on the declarations page so it does not silently fall off later.

Strategy #14: Good driver discount verification (Effort: Low | Time: 1 week | Savings: 10-20%)

This is usually a coding and eligibility verification. You can ask the carrier to verify what they view on your profile and ensure you are assigned to the right tier, as mistakes and stale pulls occur.

Strategy #15: Military and veteran discounts (Effort: Low | Time: 3-5 days | Savings: 5-15%)

If applicable, you can ask how it can be proven and if it is cumulative with other discounts.

Strategy #16: Student good grade discount (Effort: Low | Time: 1 week | Savings: 10-25%)

Submit grades, confirm when the discount expires, and note when re-verification is required so it does not disappear at renewal.

Strategy #17: Alumni and professional association discounts (Effort: Low | Time: 3-7 days | Savings: 5-10%)

Ask for the carrier’s eligibility list and cross-check your memberships. These discounts are rarely offered unless you request them.

Strategy #18: Safety feature discounts (anti-theft, airbags) (Effort: Low | Time: 1 day | Savings: 5-10%)

Most features should be captured by VIN decoding, but it is worth confirming. If something is missing, ask how to update the vehicle profile.

Where your state rules can change the outcome

Discounts are not purely carrier policy; some states set the rules. California is a good example because good-driver treatment is tightly regulated, so eligibility should be coded correctly if you meet the criteria. New York is the opposite type of constraint, where defensive driving discounts follow specific course and documentation standards. Florida shows the regional angle: some carriers apply underwriting credits or adjustments tied to storm exposure and local risk, so asking what is available where you garage the car can matter more than it would in a low-catastrophe state.

Bundle Your Policies

Bundling is one of the only ways to save money through pricing changes that won’t raise your deductibles or reduce your coverage. The multi-policy discount is a good example of this because the company knows you’ll stick around longer, file fewer claims when you have the opportunity, and be less expensive to insure as a household, so they’ll give you a better deal on the bundle than they would on a standalone car policy. The trick is to make sure the bundle is really a better deal because sometimes bundling will mask an expensive homeowners or renters policy that negates any savings on the car.

Strategy #19: Home + auto bundle (Effort: Medium | Time: 1-2 weeks | Savings: 15-30%)

This is usually the highest-impact bundle. Compare the combined total cost of both policies against your current setup, and confirm the home policy is not quietly raising deductibles or removing important endorsements just to win the quote.

Strategy #20: Renters + auto bundle (Effort: Low | Time: 3-7 days | Savings: 10-20%)

Renters insurance is usually very affordable, so the discount for having a car can pay for the cost of the additional insurance itself. It also provides a good means of protecting one’s personal property and liability, which many car owners do not realize until it is too late.

Strategy #21: Life insurance bundle (Effort: Medium | Time: 2-3 weeks | Savings: 5-12%)

Some carriers offer small bundling credits for adding life insurance. Treat this as a secondary savings lever, not a reason to buy life insurance you do not need. If you are already shopping for coverage, it can reduce auto cost slightly, but the decision should be driven by the life policy value first.

Make Sure You’re Not Overpaying

You’ll be redirected to our partner’s site to get offers.

Advertiser Disclosure

RoadBuddy is a free resource that helps drivers compare auto insurance options.

We may receive compensation from some insurance companies and partners when you click on links or request a quote through our site. This may affect where offers appear, but it does not influence our reviews, guidance, or editorial decisions.

Our content is researched and written independently to give you clear and unbiased information.

By using RoadBuddy, you acknowledge and accept this disclosure. Learn more.

Complete Defensive Driving Courses

A defensive driving discount is one of the more organized ways to get a discount because it is based on a completion certificate, not a personal guarantee to improve your driving. The problem is that it will only apply if the course is on your state’s approved list or your insurance company’s approved list, and the regulations differ greatly from state to state. In some states, it is an available discount, while in others it is available to certain age groups, and in a few others it is associated with certain programs or licensing requirements.

Strategy #22: State-approved online courses (Effort: Medium | Time: 4-8 hours | Savings: 5-15%)

Pick a class that is recognized by your state or carrier, finish it, and then submit the certificate to your carrier and verify that the discount reflects on the declarations page. You can also ask how long the discount will be valid for and if you will need to take the class again every few years to maintain the discount.

Strategy #23: Senior driver improvement courses, typically 55+ (Effort: Medium | Time: 6-8 hours | Savings: 5-20%)

Many insurers offer a larger or more consistent discount for senior driver programs, but eligibility and course requirements can be stricter. If you qualify, this is usually one of the better “time-for-savings” trades because it can reduce the premium for multiple renewal cycles.

State-specific note that actually matters here: some states mandate discounts for approved courses, while others leave it entirely to insurers, which is why the same completion certificate can produce a solid reduction in one state and almost nothing in another.

Payment and Billing Optimization

Billing choices do not change your risk, but they can change what you pay because carriers charge for installment processing and because missed payments trigger expensive penalties. This is one of the easiest sections to implement because it is administrative, not behavioral, and the savings tends to be predictable.

Strategy #24: Pay annually instead of monthly (Effort: Low | Time: At renewal | Savings: 3-8%)

Whether to pay car insurance annually or monthly is usually a balance between convenience and expenses. There may be installment charges included in the monthly payments, while the pay-in-full discount bonuses the insurer for reduced billing costs and minimized late payments. When money is a problem, some insurers provide two-pay or quarterly payment terms that are still cheaper than monthly.

Strategy #25: Set up automatic payments (Effort: Low | Time: Same day | Savings: 2-5%)

Discounts for auto-pay are typically not substantial, but they combine rather well with paperless and pay-in-full discounts. More significantly, auto-pay eliminates the risk of missing a due date, which may result in the cancellation of the policy.

Strategy #26: Avoid cancellation and reinstatement fees

Cancellation fees and reinstatement charges can wipe out months of savings and also leave a coverage gap that can drive up future costs. The smart play is to treat due dates as a hard deadline, verify payment method changes before renewal, and if changing insurance companies, set the new policy effective date first and then cancel the old policy to avoid a gap.

Credit Score Improvement

In states where credit-based insurance score is allowed, improving it can be one of the bigger medium-term levers because many insurers treat it as a stability signal. The fastest gains usually come from utilization and errors, not from chasing a perfect score.

Strategy #27: Pay down credit card balances (Effort: High | Time: 3-6 months | Savings: 10-30%)

Target revolving utilization first, since dropping balances often moves the needle faster than anything else.

Strategy #28: Dispute credit report errors (Effort: Medium | Time: 1-3 months | Savings: 5-15%)

Clean up wrong late payments, duplicate accounts, or outdated negative items that are still reporting.

Strategy #29: Increase credit limits (Effort: Low | Time: 1-2 months | Savings: 5-10%)

Higher limits can lower utilization, as long as spending stays flat.

Driving Record Improvement

A clean driving record is still the most durable way to lower premiums because it affects both surcharges and eligibility for preferred pricing tiers. A single ticket can trigger a traffic ticket insurance increase, but the bigger cost is how long it follows you in pricing. Most insurers use a lookback window in the three to five year range for common violations and at-fault accidents, which is why the savings from fixing your record often shows up later, not immediately.

Strategy #30: Let violations age off (Effort: Low | Time: 36-60 months | Savings: 20-40%)

If you already have violations on file, time is often the largest lever. As incidents age out of the surcharge window, many drivers move back into better tiers, especially if they avoid new activity.

Strategy #31: Use traffic school to remove or reduce tickets (Effort: Medium | Time: 8-12 hours | Savings: 10-25%)

Some states permit eligible drivers to remove some offenses from their record, reduce points, or suppress insurance reporting if they finish an approved course. The value is greatest in preventing the surcharge from being assessed in the first place.

Strategy #32: Enroll in an accident forgiveness program (Effort: Low | Time: 1-2 months | Savings: Varies)

Accident forgiveness is not retroactive and is not free, but it can help prevent a future at-fault accident from resulting in a large surcharge assessment. It is best for drivers who already have good rates and want to maintain them.

Strategy #33: Contest unfair tickets (Effort: High | Time: 2-6 months | Savings: 15-30%)

If the ticket is unfair, contesting it may be a good idea because a dismissal or reduction can save you from higher rates for years to come. This is best done if you have evidence, a clean record, or a good chance of negotiating it down to a non-moving violation.

Telematics and Usage-Based Insurance

Usage-based insurance is one of the few pricing mechanisms that can re-rate you based on how you drive, not who you are. It typically works best for low-mileage drivers who don’t brake hard, accelerate quickly, drive late at night, or sit in congested traffic, as these behaviors are likely to be penalized as higher risk. The catch is that you are essentially agreeing to be monitored through a safe driving app or device, and the discount is earned, not guaranteed, so it is best to approach the first term as a trial.

Strategy #34: Progressive Snapshot (Effort: Low | Time: 90-day trial | Savings: 10-30%)

Snapshot usually employs a trial period to evaluate driving habits before applying the discount. The greatest results are normally achieved through consistent and predictable driving habits and a reduced number of high-risk time-of-day trips.

Strategy #35: Allstate Drivewise (Effort: Low | Time: 90 days | Savings: Up to 40%)

Drivewise is intended to encourage more positive driving habits and may be particularly beneficial to drivers who maintain a low level of phone distraction and do not drive aggressively.

Strategy #36: State Farm Drive Safe and Save (Effort: Low | Time: 90 days | Savings: Up to 30%)

This plan usually takes into account both mileage and driving behavior, making it a good choice for drivers who have regular habits and moderate mileage.

Strategy #37: Metromile pay-per-mile, best for low mileage drivers (Effort: Medium | Time: 30 days | Savings: 20-50%)

Pay per mile insurance turns the model on its head: you pay a base rate plus a fee per mile driven, so the savings are greatest if you drive very few miles. It is not as beneficial for commuters, but it could be a huge benefit for city dwellers, telecommuters, and families with a second car that drives very few miles.

Make Sure You’re Not Overpaying

You’ll be redirected to our partner’s site to get offers.

Advertiser Disclosure

RoadBuddy is a free resource that helps drivers compare auto insurance options.

We may receive compensation from some insurance companies and partners when you click on links or request a quote through our site. This may affect where offers appear, but it does not influence our reviews, guidance, or editorial decisions.

Our content is researched and written independently to give you clear and unbiased information.

By using RoadBuddy, you acknowledge and accept this disclosure. Learn more.

Life Changes and Updates

The largest price falls are often when your risk profile changes on paper, even if your driving hasn’t. Insurers price life changes because they are associated with claim frequency and stability, so it is worth considering updates as same-day admin tasks rather than things to remember at renewal.

Strategy #38: Get married (Effort: N/A | Time: N/A | Savings: 5-15%)

A marriage insurance discount is common because married drivers are often rated as lower risk on average. Not every state or carrier uses it, but where it applies it can reduce the premium without changing coverage.

Strategy #39: Update marital status immediately (Effort: Low | Time: Same day | Savings: 5-15%)

If your marital status changed and your insurer is still rating you as single or unknown, you may be paying the wrong tier. Update it as soon as it happens and confirm it shows on the declarations page.

Strategy #40: Wait until you’re 25 (Effort: N/A | Time: N/A | Savings: 10-20%)

Age insurance rates often improve as experience accumulates. Turning 25 is not something you can change overnight, but it often aligns with how insurers model young driver risk tapering off, especially when the record is clean.

Strategy #41: Remove young drivers when they move out (Effort: Low | Time: 1 day | Savings: 15-30%)

If a young driver no longer lives with you and no longer regularly drives the insured vehicles, updating the household driver list can materially reduce cost. Do it correctly, because insurers may require proof of separate residence or separate insurance to remove them.

Long-Term Strategic Plays (6+ Months)

Vehicle Selection Strategy

If you want the biggest structural drop in premiums, it often comes from the car itself. Insurance cost by car model is not a minor detail. It is one of the inputs that follows you for years, because the insurer is pricing expected payout costs tied to that vehicle: repair severity, parts pricing, labor time, total-loss likelihood, injury outcomes, and theft exposure. That is why two drivers with similar profiles can see very different vehicle insurance rates simply based on what is in the driveway.

Strategy #42: Choose vehicles with low insurance costs (Effort: High | Time: When buying | Savings: 20-50%)

When shopping, treat insurance as part of the purchase price. Ask for quotes on the exact VIN or trim you are considering, not just the model name, then compare the annual premium difference across options. Cheap cars to insure are usually those with moderate replacement value, strong parts availability, and straightforward repairs, not necessarily the cheapest sticker price.

Cheapest cars to insure in 2026

- Hyundai i10

- Volkswagen Polo

- Skoda Fabia

- Kia Picanto

- Toyota Aygo X

- VW Caddy

- Fiat 500

- Dacia Sandero

- Renault Clio

- Seat Arona

Strategy #43: Avoid high-theft targets (Effort: High | Time: When buying | Savings: 10-25%)

Theft patterns are model-specific and can push comprehensive pricing up sharply. If a vehicle is a known high-theft target in your region, you can end up paying an ongoing penalty that has nothing to do with how you drive. When you are narrowing choices, check whether a model has elevated theft attention and price it accordingly.

Strategy #44: Consider safety ratings impact (Effort: High | Time: When buying | Savings: 5-15%)

Better safety performance can reduce injury losses, but it can also raise repair costs when a crash happens, so the impact is not one-directional. The practical play is to favor vehicles with strong crash-test performance and widely available parts, while avoiding trims that turn minor hits into expensive sensor and calibration work.

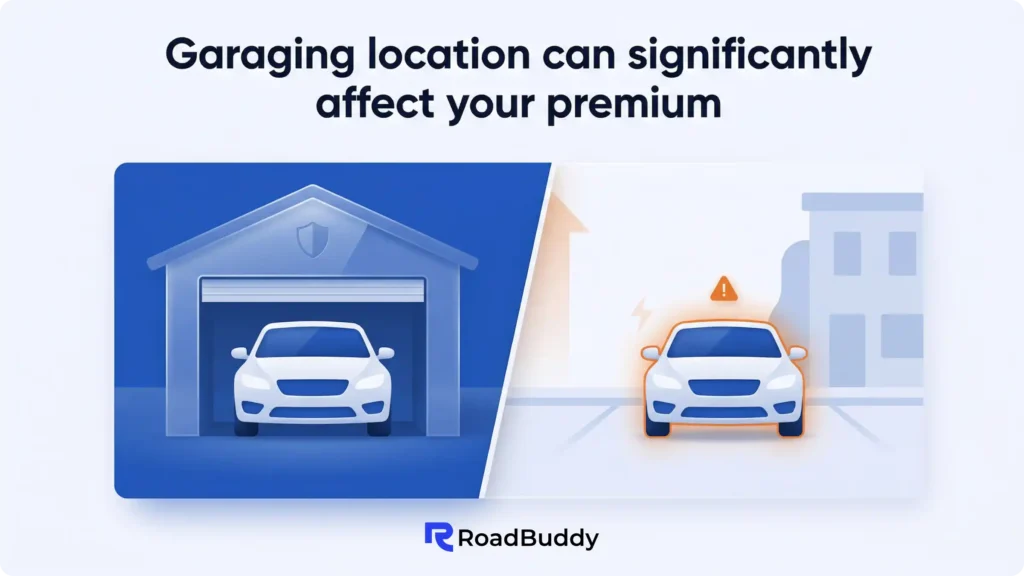

Location and Garaging

Car insurance by zip code is real because territory is a proxy for the claims environment around you: theft frequency, crash density, repair pricing, medical costs, and local legal patterns. That is why urban vs suburban insurance rates can diverge even when the driver and vehicle are the same, and it is also why relocating can change premiums more than most “discount hunting” ever will.

Strategy #45: Move to lower-cost areas (Effort: Very High | Time: 6+ months | Savings: 15-40%)

This is a long-term lever, not a tactical move, but it is one of the few changes that can reset your baseline pricing tier. If you are already considering a move, run quotes using the new garaging address before you commit, because two neighborhoods a few miles apart can price differently.

Strategy #46: Garage your vehicle (Effort: Medium | Time: Immediate if available | Savings: 5-10%)

Where the car is kept overnight matters. A locked garage or secured parking reduces theft and vandalism exposure, which can lower comprehensive costs and sometimes overall premiums. Make sure the garaging address and parking description match reality, because insurers can verify location after a claim and misrepresentation can create problems when you need coverage most.

Coverage Strategy Evolution

Insurance coverage needs change as your car and finances change, and keeping the same setup for years is how people overpay. The long-term goal is to protect the losses that would actually hurt you, while trimming coverage that no longer makes economic sense.

Strategy #47: Increase liability, drop collision as the car ages (Effort: Low | Time: Annual review | Savings: 10-30%)

As a vehicle depreciates, collision coverage often becomes a weaker value because the maximum payout shrinks while you still pay the premium and the deductible. Over time, many drivers get more leverage from increasing liability limits than from continuing to insure a low-value car for collision, because liability is what protects your assets and income if you seriously injure someone or damage expensive property. This is a cost-benefit analysis: if the car’s realistic payout minus deductible would not change your situation, collision may be optional, while higher liability limits can prevent financially catastrophic out-of-pocket exposure.

When to drop comprehensive coverage

Comprehensive insurance is usually more affordable than collision and will cover theft, weather, vandalism, and animal damage, so it can be a better value for a longer period of time. It becomes less desirable when the car is worth less, the chances of theft are low in your area, and you can afford to buy a new car without breaking the bank. If comprehensive insurance is only paying out a small claim amount, then you are essentially paying for the benefit of having it.

Make Sure You’re Not Overpaying

You’ll be redirected to our partner’s site to get offers.

Advertiser Disclosure

RoadBuddy is a free resource that helps drivers compare auto insurance options.

We may receive compensation from some insurance companies and partners when you click on links or request a quote through our site. This may affect where offers appear, but it does not influence our reviews, guidance, or editorial decisions.

Our content is researched and written independently to give you clear and unbiased information.

By using RoadBuddy, you acknowledge and accept this disclosure. Learn more.

Umbrella policy cost-benefit analysis

An umbrella policy is an umbrella over your auto and home/renters liability limits and may be a very economical way to purchase an extra layer of coverage, particularly if you have assets, higher income, or higher lawsuit exposure. It typically demands higher underlying liability limits, but the marginal cost of additional protection per dollar may be attractive compared to extending auto liability limits to very high levels.

Savings Stack Combinations: High-Impact Stacks by Profile

The fastest way to maximize insurance discounts is to stack a few compatible moves that hit different parts of the pricing formula at once, rather than chasing one discount in isolation. These car insurance savings combinations are built as plug-and-play profiles, so you can copy the stack that matches your situation and implement it in one cycle.

Stack 1: Young Driver (18-25)

Start with the big levers that insurers price most aggressively for young drivers: eligibility discounts plus structure. The most reliable stack is a good student discount layered onto a parent’s policy (when the household setup is legitimate), then add telematics and a defensive driving course where it is recognized. This combination works because it offsets the young-driver risk tier with documented signals that reduce expected losses, and it often beats trying to buy a stand-alone policy at 18-25.

Total potential savings: 40-60%

Stack 2: Work-From-Home Professional

This profile wins by attacking exposure. Report reduced mileage, then choose either usage-based insurance or pay-per-mile if you drive very little. Add a multi-policy bundle (renters or homeowners) to capture the retention discount without changing coverage quality. The key is keeping the coverage consistent while you re-rate the mileage and usage assumptions that were built for commuting drivers.

Total potential savings: 35-55%

Stack 3: Senior Driver (65+)

This stack is about verified eligibility and predictable billing credits. Use an AARP discount or equivalent affinity discount if your carrier honors it, complete a senior driving course for the structured reduction, and ask for a rate review to confirm you are in the correct tier. Pair it with annual payment to reduce installment fees and lower lapse risk.

Total potential savings: 30-45%

Stack 4: New Homeowner

New homeowners have a natural bundling advantage. Start with a home and auto bundle, then increase deductibles to reduce the physical-damage premium while the home policy is already being rewritten. Add automatic payments to pick up billing discounts and reduce cancellation risk. If credit improvement is realistic, this is one of the best profiles for medium-term savings because homeownership and credit signals often stack well in underwriting.

Total potential savings: 40-65%

Stack 5: Rural Driver with Older Vehicle

This is the classic “stop overinsuring the asset” profile. Drop collision, keep liability strong, and set a high deductible comprehensive if theft and weather risk still justify comp. Add multi-car if available and confirm low mileage bands, since rural drivers often drive fewer stop-and-go miles even when distances are longer. The savings comes from removing the most expensive part of full coverage while keeping protection against losses that would be financially painful.

Total potential savings: 45-70%

Stack 6: Urban Driver Minimal Use

Urban minimal-use drivers often benefit most from pricing structures that charge by usage. Use usage-based insurance or pay-per-mile, and match coverage to actual exposure while staying legal in your state. If you rely on ride-share or public transit most days, coordinate your driving patterns so the insured vehicle is truly low-mileage rather than “sometimes a commuter car.” The savings here comes from aligning premium with real usage and avoiding paying commuter rates for a parked car.

Total potential savings: 50-75%

State-Specific Strategies: Top States with Unique Opportunities

California

California is one of the few big states where rate changes run through a prior-approval system under Proposition 103, which gives consumers more leverage when pricing gets aggressive. It also has a true good-driver framework: if you qualify, the good driver discount must be at least 20% below the comparable non-good-driver rate, so it is worth confirming you are coded correctly. California’s rules also narrow what insurers can rely on in rating, which is why shopping can look different here than in most states.

Texas

Texas is a volume market with lots of carrier options, which makes compare car insurance quotes especially productive at renewal time and after life changes. Defensive driving discounts are commonly available, but eligibility and discount size vary by insurer, so it only works if you confirm the course is accepted before you take it. Texas is also a strong state for regional carriers, and an independent agent can often surface options that do not show up in direct online shopping.

Florida

The Florida baseline is informed by its no-fault profile. Motorists are required to carry PIP and property damage liability in order to register their vehicles, and the presence of the PIP layer affects how claims for injuries are paid and priced. Opportunities are likely to arise from narrowing the options for coverage (notably comp and collision deductibles), locking in discounts related to senior plans, and thinking carefully about comprehensive coverage in a state where storm and flood claims are part of the pricing context.

New York

New York has one of the cleanest, most reliable discount mechanisms in the country through the DMV’s Point and Insurance Reduction Program. If you are the principal operator and complete an approved course, the insurer applies a 10% premium reduction, and the state rules around eligibility are straightforward. New York is also highly regional in pricing, so shopping within the same coverage structure matters because small territory differences can translate into big premium differences.

Pennsylvania

Pennsylvania gives drivers unusually direct levers to trade price for legal rights and protection. The limited tort versus full tort choice can reduce premium, but it also limits your ability to recover for pain and suffering in many situations, so it is a true cost-benefit decision rather than a free discount. Pennsylvania is also a state where stacked versus unstacked UM/UIM decisions matter; stacking increases protection across vehicles, while unstacking can reduce cost.

Illinois

Illinois is a good example of a state where non-driving factors can materially influence pricing, including the use of credit-based insurance scoring, so improving credit inputs can translate into premium movement over a few months. On the discount side, insurers commonly recognize approved defensive driving courses, especially for older drivers, but you still need to confirm your carrier’s acceptance and documentation rules before you take a class.

Make Sure You’re Not Overpaying

You’ll be redirected to our partner’s site to get offers.

Advertiser Disclosure

RoadBuddy is a free resource that helps drivers compare auto insurance options.

We may receive compensation from some insurance companies and partners when you click on links or request a quote through our site. This may affect where offers appear, but it does not influence our reviews, guidance, or editorial decisions.

Our content is researched and written independently to give you clear and unbiased information.

By using RoadBuddy, you acknowledge and accept this disclosure. Learn more.

Common Mistakes and Pitfalls: What Not to Do

The costliest car insurance blunders typically involve trying to find the lowest number in a way that ultimately puts you at risk down the line. Cutting back on necessary coverage to meet a budget goal can leave you inadequately insured when a serious accident occurs, particularly if you forgo uninsured motorist coverage in a state where hit-and-run and low-limit drivers are prevalent. Budget savings should result from better design, not from stripping away the protections that prevent financial harm.

Gaps in coverage are another frequent insurance mistake. A missed payment, a late renewal, or failing to cancel your previous policy before activating the new one can result in a gap that increases your premiums for months or even years. View continuous coverage as a kind of insurance credential. When changing insurers, list the new policy first and then cancel the old one after verifying the start date to avoid any gaps.

Do not lie about mileage or garaging. It is tempting because it looks like an easy discount, but it crosses into misrepresentation and can create claim problems when the insurer verifies where the car is kept or how it is used. Also do not ignore state minimum requirements, because saving money by going below legal limits is not a strategy, it is a future legal and financial problem.

Finally, avoid combining strategies that cancel each other out. For example, paying for low deductibles while also trying to cut costs through removing collision often produces a messy policy that is neither cheap nor protective. And do not skip shopping at renewal. Even one comparable quote check per year is enough to catch when your carrier drifted out of the competitive range.

Action Plan Template: Your Savings Roadmap

Compare at least five quotes with the same limits and deductibles, update your annual mileage and usage, increase deductibles only if you have enough in your emergency fund to cover them, eliminate small endorsements you do not use, such as rental or roadside assistance if you have other options, check all discounts listed on your declarations page, enable paperless and auto-pay if offered, and check for errors in drivers, vehicles, and garaging address.

Run a full discount audit including affiliations, student or military eligibility, and safety features, explore bundling options for renters or home, consider a defensive driving course if your state and carrier recognize it, request a rate review to confirm you are in the right tier, evaluate whether collision still makes sense for older low-value cars, check whether pay-in-full reduces installment fees, test a telematics program if your driving patterns fit, and document what changed so renewal comparisons are clean.

Reduce credit utilization and correct credit report errors where credit-based scoring is used, manage claims strategy by paying small losses out of pocket when rational, keep your driving record clean and address eligible tickets through traffic school where allowed, and re-quote after any life change like marriage, a move, or a driver leaving the household.

Choose your next vehicle with insurance cost by model as a purchase factor, tighten coverage strategy as the car depreciates by keeping strong liability while trimming collision when it stops making sense, and re-evaluate where the car is garaged and whether a secure parking change is feasible.

FAQs

For most people who actively shop and optimize, they can find savings in the 10% to 40% range, and higher if you are currently priced poorly or have mismatched coverage. Your upside will depend on your state, driving record, credit-based scoring rules, vehicle, and market competitiveness.

Yes, when the annual savings advantage clearly outshines the hassle and loss of benefits. The simplest break-even analysis is to determine if the difference is still significant after you check the same limits and deductibles, and after you enter any cancellation fee or loss of accident forgiveness benefits.

At least once a year, and whenever a trigger event occurs: renewal, move, marriage, new car, addition or deletion of a driver, or large mileage increase.

Often, but not necessarily automatically. Many surcharges remain in effect for three to five years, but you may need to shop or ask for a re-rate to ensure the old ticket or accident is no longer impacting your rate level.

Unlike conventional negotiating, you can achieve an outcome through a discount audit, verification of rating inputs, and the use of competing quotes to gain access to retention pricing if it is available.

No. Bundling can backfire if the home or renters policy is overpriced or has worse deductibles and endorsements. Always compare the combined total cost of both policies against buying each separately.

Getting similar quotes is typically where the highest hourly savings are. Next would be the best wins from deductibles, coverage fit, especially collision on older vehicles, mileage accuracy, and discount checks.

They are usually close, but the final price can change after verification of driving record, claims history, credit-based insurance scoring where used, mileage, garaging address, and VIN details.

In most states, insurers employ the use of credit-based insurance scoring, which may significantly affect premiums. Higher utilization or missed payments may increase premiums despite flawless driving, while in some states, the use of credit is prohibited or restricted.

Typical misses include low-mileage bands, affiliation or employer discounts, student good-grade, defensive driving, safety and anti-theft features not accurately reflected, multi-policy alignment, and paid-in-full credits. Discounts can be stacked or offset one another.

It can be if you have low mileage and are a smooth driver, as the savings can be substantial. It all comes down to your comfort level with data collection, what is collected, how long it is retained, and whether you can opt out later with no penalty.

If you have a loan or lease, you cannot. If you own your vehicle outright, you may want to cancel collision coverage when the annual premium and deductible add up to a large percentage of the vehicle’s value, and keep comprehensive coverage longer if theft and weather are significant.

They estimate the claim frequency and severity based on your characteristics and geographic location, and then use filed rates based on characteristics such as driving record, vehicle, territory, mileage, and in some cases, credit-based insurance scores, and finally add in operating costs.

Typically only if you are still considered to be part of the household under the rules of that carrier, such as a college student away at school. Otherwise, you may need to purchase your own policy or a named driver agreement that meets the carrier’s requirements.

It can put you into higher levels of insurance, cause reinstatement problems, and sometimes additional filings depending on your state and circumstances. It is one of the fastest ways to increase the price of future insurance.

Yes, it often does. There are usually installment fees or additional costs built into the monthly payment plans, so paying annually or making more payments can save you money.

Sometimes, especially in states where they specialize and price aggressively. The trade-off is checking financial strength and complaint patterns, since service quality matters most when you file a claim.

Typically three to five years for pricing, but it depends on the state and the company, and serious infractions may impact eligibility beyond the surcharge period.

You will need at least what your state requires, but many people find value in higher liability limits than the minimum, as well as UM/UIM if offered, and comp/collision depending on the value of your car and your financial ability to absorb a loss.

Yes. Most policies will refund on a prorated basis, although some companies use short-rate calculations in specific situations. The best practice is to begin the new policy and then terminate the old one to ensure there is no lapse in coverage.

Table of contents

Looking for Auto Insuranse?

Make sure you’re not overpaying

You’ll be redirected to our partner’s website to compare personalized offers.

Advertiser Disclosure

RoadBuddy is a free resource that helps drivers compare auto insurance options.

We may receive compensation from some insurance companies and partners when you click on links or request a quote through our site. This may affect where offers appear, but it does not influence our reviews, guidance, or editorial decisions.

Our content is researched and written independently to give you clear and unbiased information.

By using RoadBuddy, you acknowledge and accept this disclosure. Learn more.